Financing Option

Equipment Loans

Equipment loans give you full ownership from day one while spreading the cost across 24 to 84 months. We specialize in production-line assets from $50k to $5M+.

Start Review

A line is only as fast as its slowest station, so the smart spend is the one that clears the bottleneck first. An equipment loan does exactly that: it puts the asset on your floor, under your control, from the day the ink dries. You own the machine, you depreciate it, and the payment runs fixed for the life of the term. There is no residual to negotiate, no lessor to call for permission to modify tooling, and no balloon you have to plan around at month 48.

We work with manufacturers, co-packers, automotive suppliers, plastics processors, and food producers who need capital deployed at the pace the line demands. Our minimum is $50,000, the sweet spot is $100,000 to $5,000,000 or more, and most of our borrowers fund within one to two weeks of a completed application. If throughput is the goal, ownership is usually the fastest path to OEE improvement because you control the asset entirely.

How a Production-Line Equipment Loan Works

An equipment loan is a secured term loan where the machine itself serves as collateral. We advance the purchase price, you take title, and you repay in fixed monthly installments over a negotiated term. Terms commonly run 24 to 84 months depending on the asset's useful life and your cash-flow profile.

The interest rate is fixed at origination, so your cost per unit produced is predictable from month one. On large transactions, we sometimes request three months of business bank statements. On requests up to roughly $400,000, we can often move with an application and basic equipment details, which compresses the diligence cycle considerably for buyers who need to close before a vendor slot disappears.

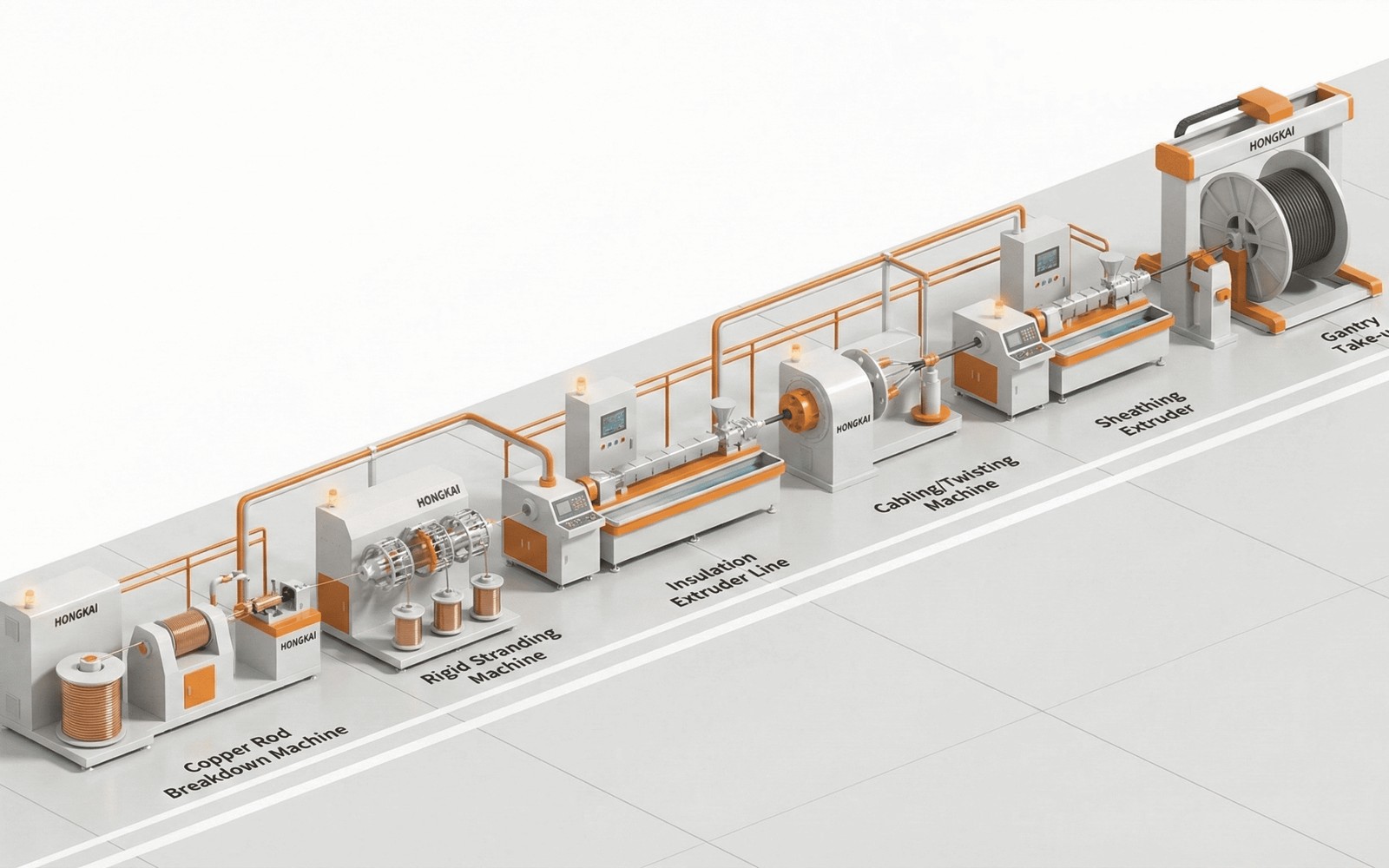

Collateral is the equipment. We do not take a blanket lien on your entire business for a single-machine transaction. For complete-line projects, we structure accordingly, but the point is that the underwrite stays proportional to the asset. If you are financing Conveyor System Financing or an integrated Automated Assembly Systems Financing, the loan can cover the full installed project cost, including installation labor, controls, and startup commissioning, as long as those costs are documented on the invoice.

What Production Equipment Qualifies

Our loan programs cover the full range of manufacturing and processing assets: filling lines, blow-molding equipment, thermoformers, robotic cells, palletizers, vision systems, checkweighers, injection molding presses, extrusion lines, CNC machining centers, and complete integrated systems. Both new and quality-used equipment qualify.

For used assets, we look at age relative to the asset type. A five-year-old Robotic Assembly Cell Financing from a reputable integrator often carries most of its useful life ahead of it and finances well. A 20-year-old single-purpose press in a shrinking market is a different conversation. The practical guideline: if the asset has a clear secondary market and a realistic service life extending past the proposed loan term, it qualifies.

We regularly finance equipment for Food & Beverage Manufacturing, Contract Packaging & Co-Packers, pharmaceutical producers, and automotive-parts suppliers. The industry matters less than the underlying asset quality and the borrower's repayment capacity.

Terms, Rates, and What Drives Your Payment

Three variables set your monthly payment: the loan amount, the term length, and the rate. Rate is driven by business credit, time in business, financial performance, and the residual value of the equipment. Stronger borrowers on bankable assets get competitive rates. B and C credit borrowers pay a premium, but they still get funded on assets that support the advance.

Term length is where you have the most leverage. A shorter term builds equity faster and costs less total interest. A longer term reduces the monthly payment and preserves operating cash flow, which matters if you are simultaneously funding a staffing ramp or a raw-materials build. Most plant operators targeting throughput improvements pick the term that keeps the monthly payment inside the incremental gross profit the equipment generates, so the line pays itself before the loan does.

Rates are not something we publish because they move with market conditions and borrower profile. What we can say is that we do not pad origination with hidden fees. You see the total cost before you sign, and you can prepay without a penalty on most structures. If you want a quote, the fastest path is submitting an application with the asset invoice or description and letting us run the numbers.

Buying New vs. Used on a Loan

New equipment carries OEM warranty coverage, current controls architecture, and often faster parts availability, which translates directly to uptime. The cost is higher, but the loan tracks the asset's actual value more closely because there is no prior usage depreciation to discount. Banks and institutional lenders prefer new-iron transactions, so borrowers with strong credit get their best pricing on new assets.

Used equipment bought well can clear a bottleneck at half the cost of new, which changes the ROI math substantially. A reconditioned Packaging Line Financing from a reputable dealer, inspected and with a short parts warranty, might fund a project that a new-equipment quote would have pushed out 18 months while capital accumulated. We finance used production equipment routinely, and we have no prejudice against it so long as the asset condition and age support the advance amount.

The decision really comes down to throughput timing and capital cost. If waiting for new delivery slots costs you a contract, the right used asset funded today is often the correct call. If the downtime risk on older equipment would offset the savings, new financing wins. We help you think through that tradeoff before you commit.

Questions About Equipment Loans

Clear answers on equipment eligibility, documentation, timing, and transaction structure before you send the file.

Can I include installation and commissioning costs in the loan?

Yes, as long as those costs appear on a vendor invoice or project contract. We can advance against documented soft costs tied to the equipment project, including integration labor, controls programming, and startup support. Equipment-only advances are also available if you prefer to separate the capital spend.

Does the loan cover used production equipment, or only new?

Both. Used equipment qualifies when the asset age, condition, and secondary-market value support the advance. For most industrial production assets, equipment under ten to twelve years old in verifiable working condition finances without issue. Older equipment is evaluated case by case based on remaining useful life.

How quickly can we close if I have a vendor holding a machine for me?

On application-only transactions up to roughly $400,000, we typically close within five to seven business days of a completed application. On larger transactions requiring financials, plan on one to two weeks from the day we receive a complete package. Letting us know there is a hard deadline on vendor hold moves it to the front of the queue.

Do I need a down payment?

Not necessarily. On strong credits with bankable assets, we can advance the full purchase price with no down payment. On B or C credit files or high-risk asset types, we may require 10 to 20 percent down to reduce exposure. The application tells us what structure works best for your profile.

What happens to ownership if I default?

The equipment secures the loan. In a default scenario, the lender has recourse to the asset. This is the same structure as a commercial vehicle loan. Because production equipment often retains meaningful value, lenders are motivated to work through payment hardship rather than repossess, so open communication early is always the better path.

Finance Your Equipment Loans

Send the equipment quote, seller details, price, deposit, and delivery schedule. The financing desk will review the file and return a practical next step.